AR autocorrelation

In the stationary AR(1) model the value of a is constant for all time. The statistical quantities underlying this model are constant essentially because a is constant.

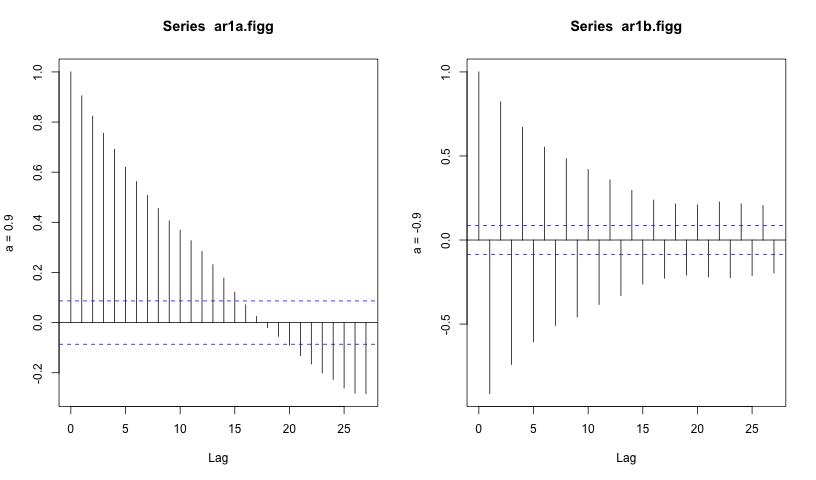

The autocorrelation function for an AR(1) process with parameter a can be shown mathematically to be equal to ak for (integer) lag k. The empirical autocorrelation functions for our two AR(1) processes, with parameters of 0.9 and -0.9 can be seen in the left and right-hand plots of the figure below. In the left-hand plot one can see that there is a high degree of linear association at small lags, whereas in the right-hand plot alternate lags result in successive negative and positive autocorrelation values.

References...

|